Claims Adjuster

In the realm of property insurance claims, few issues are as complex and potentially hazardous as those involving lead paint and asbestos. These harmful materials, once commonly used in construction up until 1980, have since been recognized as serious health risks. The discovery of asbestos or lead paint can lead to myriad legal and financial challenges for both property owners and insurance companies. When you work as a claims adjuster, navigating these complex challenges requires a deep understanding of the hazards, regulations, and best practices involved in handling asbestos and lead paint claims.

In the realm of property insurance claims, few issues are as complex and potentially hazardous as those involving lead paint and asbestos. These harmful materials, once commonly used in construction up until 1980, have since been recognized as serious health risks. The discovery of asbestos or lead paint can lead to myriad legal and financial challenges for both property owners and insurance companies. When you work as a claims adjuster, navigating these complex challenges requires a deep understanding of the hazards, regulations, and best practices involved in handling asbestos and lead paint claims.

The Menace of Lead Paint and Asbestos

Asbestos and lead paint are two notorious substances that were once commonly used in construction, but are now recognized as hazardous due to their severe health risks. Asbestos, a mineral fiber known for its heat- and fire-resistant properties, was used in various building materials such as siding, undersheeting, insulation, roof shingles, textured paint, and floor and ceiling tiles. Similarly, lead paint was widely used until its dangers became evident, especially for young children exposed to chipping or flaking paint.

Exposure to asbestos fibers and lead particles can lead to a range of serious health issues. Asbestos is a known carcinogen that can cause lung cancer, mesothelioma, and other respiratory disorders when its fibers are inhaled. Lead, on the other hand, can lead to brain and nerve disorders, developmental delays, cognitive impairments and other problems.

In fact, asbestos and lead paint are so dangerous, only certified and licensed abatement professionals are allowed to remove these substances from residential properties. Those individuals know the proper steps to take before removal of these hazardous materials. They also have the right training to completely remove all traces of asbestos and lead paint, and to ensure all fibers and dust are contained during this process.

Which Homes May Have These Dangers

The federal government banned lead-based paint from residential use in 1978. That means any home that was built before 1978 may contain lead paint. This is particularly true if the home was built before 1960.

Homes built before 1980 are suspected to contain asbestos. Some homes built during the 1980s may contain it as well, even though sales of asbestos-containing construction items were diminishing. In 1989, the Environmental Protection Agency issued a final rule banning most asbestos-containing products.

When Lead Paint or Asbestos Abatement Might Be Covered

Almost all home insurance policies exclude coverage for pollutants. Therefore, asbestos and lead-paint removal likely will not be covered unless the material was disturbed or exposed by a covered peril, such as wind or fire damage.

Homeowners who file asbestos insurance claims or lead paint insurance claims unrelated to covered perils are unlikely to receive compensation.

Your Role as an Adjuster

If you handle home-insurance claims, you will play a critical role in evaluating and processing any claims related to asbestos and lead paint. Your expertise is crucial for determining coverage and liability, which will affect the amount of compensation for affected homeowners. Here are seven best practices to follow when dealing with an older home:

1. Gather Detailed Information

When you investigate a home-insurance claim, thorough research is required. This includes collecting information about the property's history, construction materials, renovation projects, and any previous claims or repairs. Gathering this data will help you understand the potential of exposure to health dangers and also evaluate the extent of damage.

2. Assess Lead Paint and Asbestos insurance Coverage

Analyzing the homeowner’s policy is a crucial step. You should determine if the policy covers removal and remediation of asbestos and/or lead paint in relation to covered perils.

3. Inspect the Home

Conduct an onsite inspection to investigate the claim that was filed. Be sure to protect yourself with appropriate Personal Protective Equipment (PPE) to prevent exposure to asbestos and lead paint. (Don’t assume the home is free of those hazards. You can't tell just by looking at it.)

4. Create Documentation

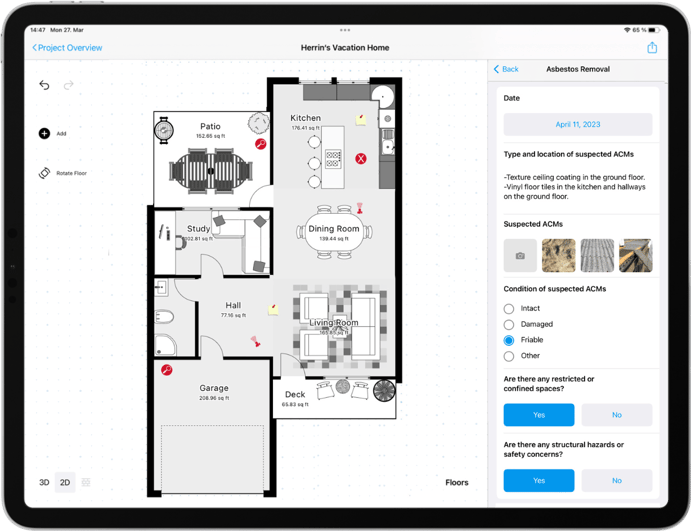

Use a mobile floor plan app, such as magicplan, to consolidate your findings with a professional approach. The app will allow you to create a sketch of the damaged area of the home easily and quickly – within just a few minutes. Then you can insert annotations and add photos to paint a detailed picture of the scene.

5. Engage Qualified Experts

If you suspect lead paint or asbestos is present, due to the age of the home, request approval to have a qualified abatement company complete an inspection. Timely action is essential. Make sure the inspection will include a complete visual examination, along with careful collection and lab analysis of samples. If asbestos or lead paint is present, the inspector should provide a written evaluation describing its location and extent of damage, and give recommendations for next steps. This information will guide you in making informed decisions regarding coverage and liability.

6. Understand the Minutia of Regulatory Compliance

You will need to have a strong grasp of federal, state, and local regulations concerning asbestos and lead paint. (Take advantage of workshops, seminars and training programs to learn more about these topics, and to ensure you are informed about any changes stemming from new legislation.) Government regulations dictate safe removal and disposal procedures, exposure thresholds, and disclosure requirements. Adhering to these rules is critical to avoid legal issues and ensure the safety of all parties involved.

7. Submit a Detailed Report

Throughout the claims process, effective communication is vital. Use your floor plan app to produce and share a photo report about your initial assessment. Be sure to include any abatement-company input and recommendations, along with your policy-coverage determination and proposed actions.

Conclusion

Residential lead paint and asbestos claims management demands a high level of expertise, sensitivity and diligence. By understanding these hazards, knowing the age of homes that might contain them, adhering to policy terms, and following best practices, you can navigate the complexities of these claims successfully. You can also take pride in knowing you are doing your part to help minimize health risks for homeowners.

EXCITING NEWS!

The magicplan app now integrates with Xactimate®

See how you can send your magicplan sketches to Xactimate in seconds

Bernd Wolfram

Head of Product

The Ultimate Guide to Succeed as a Claims Adjuster

Start refining your claim documentation process and enhance your value and reputation as a skillful claims adjuster.

.webp?width=192&height=291&name=claims%20pro%20(claims%20adjuster%20ebook%20guide).webp)

Share article